Blog

Perspectives on business valuations, litigation support, financial management, and the evolving landscape of professional accounting services.

Salmon v. Sonnet Insurance Company

The "Are You Really Self-Employed Though?" Case

A guy gets hurt in a car accident. Everyone agrees he deserves income replacement benefits. The only fight? Whether he gets $400/week (the employee rate) or $185/week (the self-employed rate). That's a $215/week difference — over five years, we're talking six figures.

Igbinobaro v. Dominion of Canada (Travelers)

When Your Story Changes Every Time You Tell It

There are LAT decisions where the applicant loses on a technicality. And then there's Igbinobaro v. Dominion, where the applicant's case collapsed under the weight of its own contradictions — and a baffling absence of documents that should have been easy to produce.

Zhu v. Co-operators General Insurance

When You Won't Show Your Tax Returns, Don't Expect a Cheque

The applicant was in a car accident. Both sides agreed he was disabled enough to qualify for Income Replacement Benefits. The only question was: how much per week? He wanted $400/week. Co-operators said: we'd love to calculate that for you, but you won't give us the documents we need to do the math.

Kfouri v. TD General Insurance Company

When Tax Filings and IRB Claims Tell Different Stories

The way you report your income to the CRA is the way your IRB will be calculated. Full stop. A $989/week vs $80/week dispute came down to a single question: T4 or T4A?

Nice Try, Counsellor: Zeineddine v. Economical Mutual Insurance Company

When You Try to Combine Two Different Rules to Create Eligibility That Doesn't Exist

The lawyer tried to thread a needle that was never threaded before — combining employment weeks and self-employment weeks to clear the 26-week IRB eligibility threshold. The Tribunal wasn't convinced. Sometimes you have to admire the creativity.

Omoruyi v. TD General Insurance Company

The Province of Ontario Likes Employees Better Than Entrepreneurs, I Guess?

A personal support worker earning $99,201 a year received an IRB of exactly zero dollars per week. Not because she wasn't injured. Not because she wasn't disabled. Not because she wasn't working. But because the Schedule's formula, applied to the specific timing of her transition from employment to self-employment, produced a number that is mathematically and practically zero.

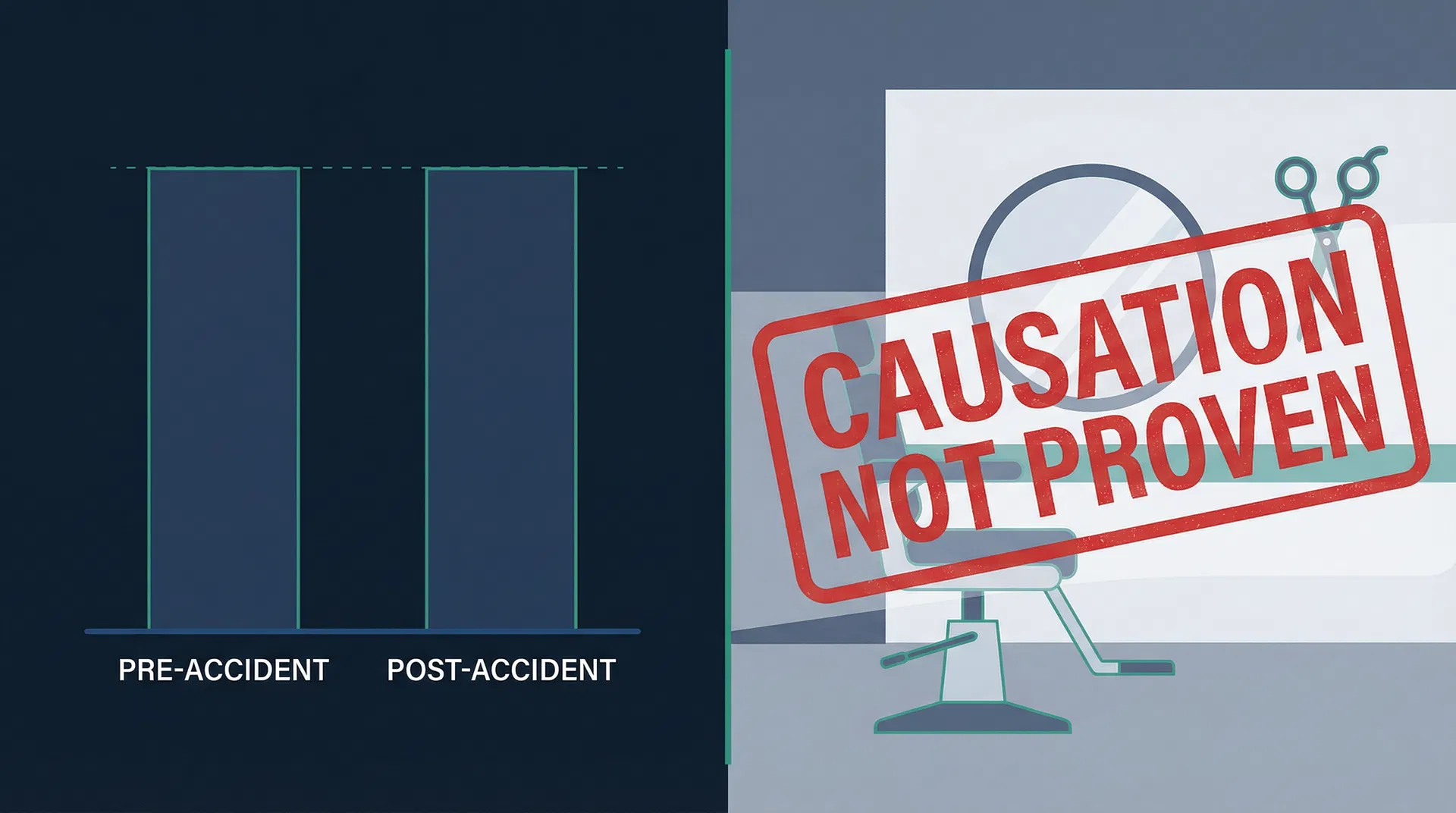

Mears (Griffiths) v. TD General Insurance Company

When Self-Employment Losses Existed Before the Accident, You Can't Just Blame the Accident

A claimant with both employment and self-employment income, where the self-employment side was already losing money before the accident. The question: can those losses be added to the IRB calculation? The Tribunal's answer: not without evidence of causation.

Get new case commentary in your inbox

No noise — just analysis when a new post goes up.